SpaceX IPO: How stable is the $1.75 trillion orbit?

The upcoming SpaceX exchange debut is setting a new valuation record. Is there any upside left for investors?

Despite making billions and being worth trillions, SpaceX still remains a startup chasing big dreams rather than optimizing for margins. We embrace that startup perspective and look inside to see whether any upside remains for IPO investors.

Key points:

Big payday for early backers

AI infrastructure and apps become the main growth drivers, guarded by space capacity and compute power moats

The long-run multiple compression is imminent, but there’s significant runway for growth thanks to a large TAM

Our verdict - below

Sending multiples to orbit

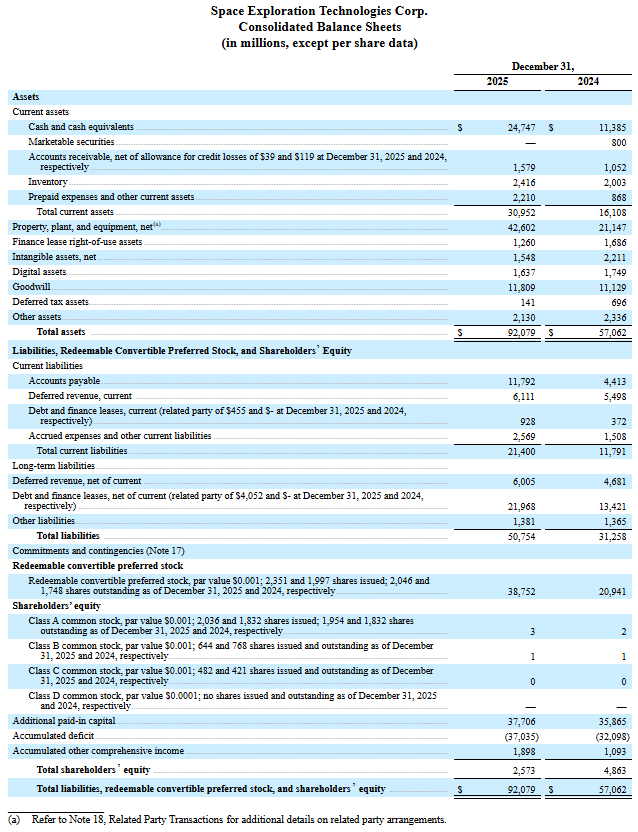

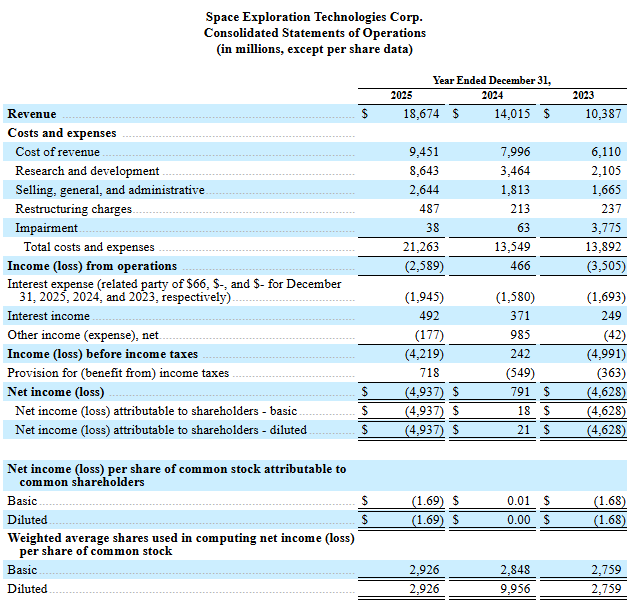

Let’s take a look at SpaceX’s financials from S-1:

Though the official price tag isn’t known yet, the company is reportedly aiming for a $75 billion raise at a $1.75 trillion valuation, which corresponds to:

$598 price per share ($1.75T / 2,926 million shares)

94x EV/S multiple ($1.75T / $18.7B revenue)

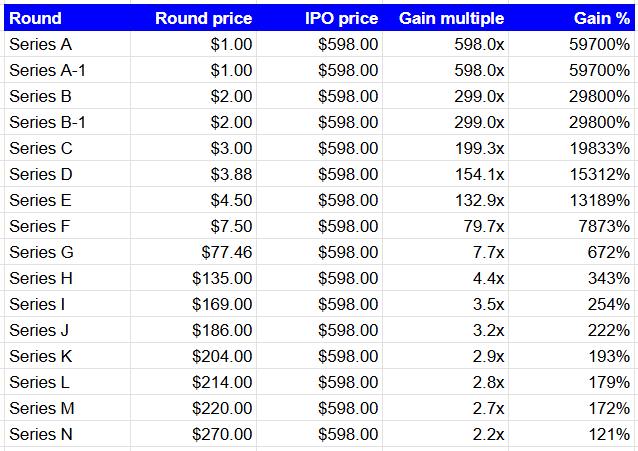

We also finally know the share prices of early funding rounds. Spoiler - early investors are taking home loads of money:

94x EV/S multiple is already in the stratosphere, and it’s a matter of time before it collapses to some long-run equilibrium, a common dynamic for tech companies after going public. To estimate the equilibrium, though, we need a peer group to compare against. Which is tricky, because after a series of mergers, SpaceX became four companies in one: an AI company (xAI), a telecommunications company (Starlink), a social media company (X.com), and - finally! - a space launch company.

How does all this fit under one roof? The company argues it’s actually one machine powered by three “foundational competitive advantages” - Space, Connectivity, and AI - that compound. The narrative: use cheap multi-use rockets to deploy satellites and space compute clusters; use the established telecom network and compute power to deliver cheap AI inference to customers on Earth (including itself); use that inference capacity to drive AI adoption at an unprecedented scale.

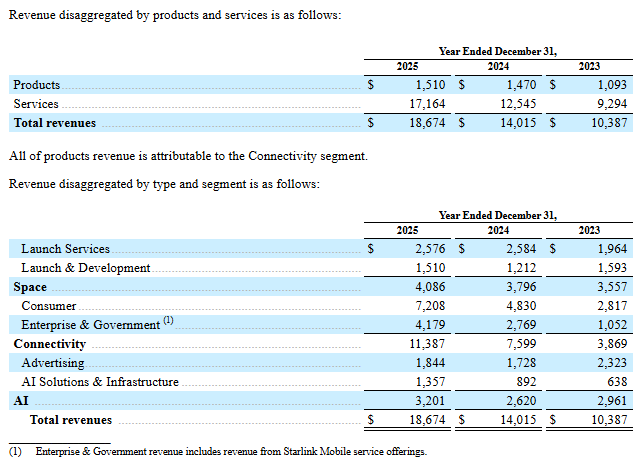

The point is, SpaceX is no longer pitching itself as a pure launch provider but as a vertically integrated infrastructure player across those three sectors, expecting most of its future growth to come from AI:

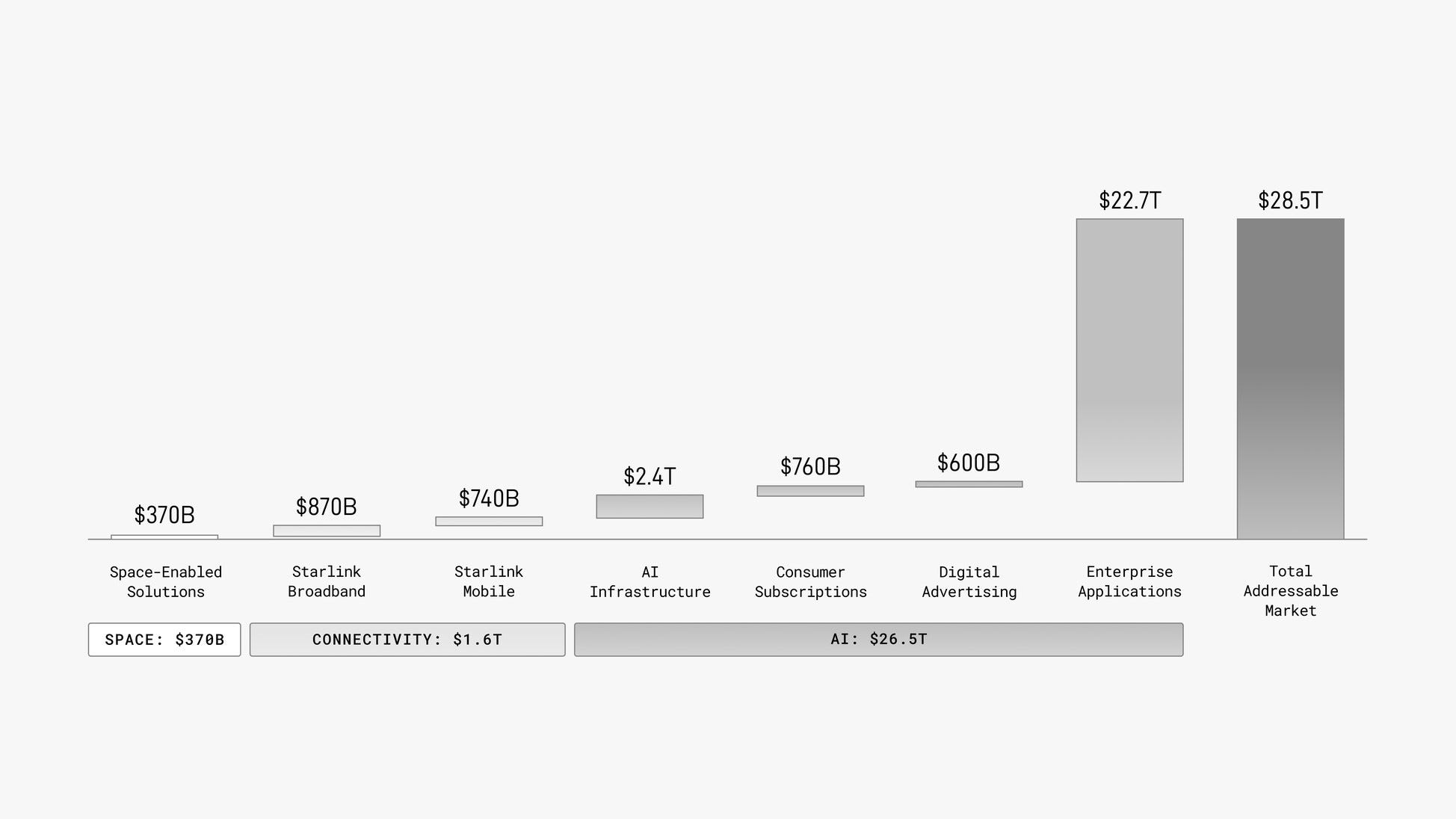

We believe we have identified the largest TAM in human history. We estimate that our quantifiable TAM is $28.5 trillion, consisting of $370 billion in Space from space-enabled solutions; $1.6 trillion in Connectivity across $870 billion in Starlink Broadband and $740 billion in Starlink Mobile as well as additional opportunities in enterprise and government; $26.5 trillion in AI across $2.4 trillion in AI infrastructure, $760 billion in consumer subscriptions, $600 billion in digital advertising, and $22.7 trillion in enterprise applications.

Within AI, the company targets two critical layers of the stack: the compute infrastructure and the front-end applications. On the compute side, it’s relying on global demand for data centers and is already renting out its Colossus cluster to Anthropic. On the applications side, it’s pushing an enterprise AI platform, Macrohard, to automate enterprise workflows and capture a slice of the impending agentic economy.

This suggests we’re evaluating an AI company. Having that figured out, we can compare SpaceX to NVIDIA (the clearest example of an AI hot stock), Tesla (included in our most recent AI stocks overview and whose valuation incorporates the “Elon Musk” factor), and the NASDAQ median (just for reference):

At those pricing levels, the only clear strategy for IPO investors to make their money back is waiting until the company outgrows the multiple compression, which seems imminent. This is similar to how venture investors view startup investing, and with startups, the long-term growth story is what matters. Let’s take a look from that angle.

Hit the target no one else can hit

Technically, startup valuation comes down to predicting:

The terminal revenue (being measured top-down as “TAM x share” or bottom-up as “units x price”)

Exit EV/S multiple (derived from where the markets have historically traded)

The probability of the terminal revenue target getting hit (this parameter is implicit, vague, and the source for most of the errors, yet the most important)

Putting everything together, Terminal Revenue * Exit EV/S multiple * Probability = Expected Enterprise Value, or E(EV). For SpaceX investors to earn anything back, that number has to be greater than $1.75T.

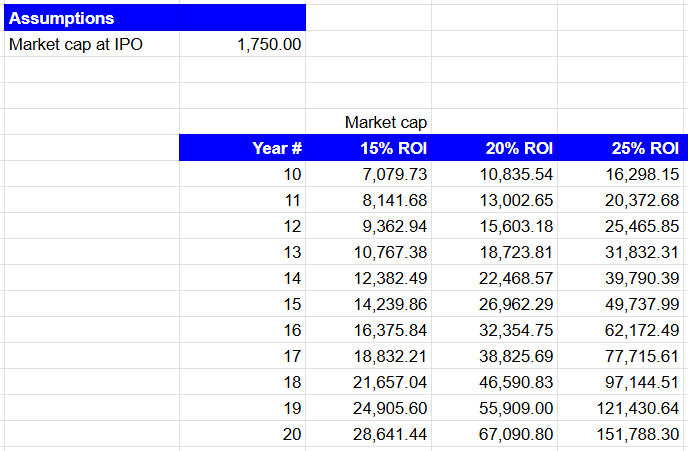

To deliver a 15-25 percent annualized return1, the company’s market cap needs to reach between $7T and $16T by 2036:

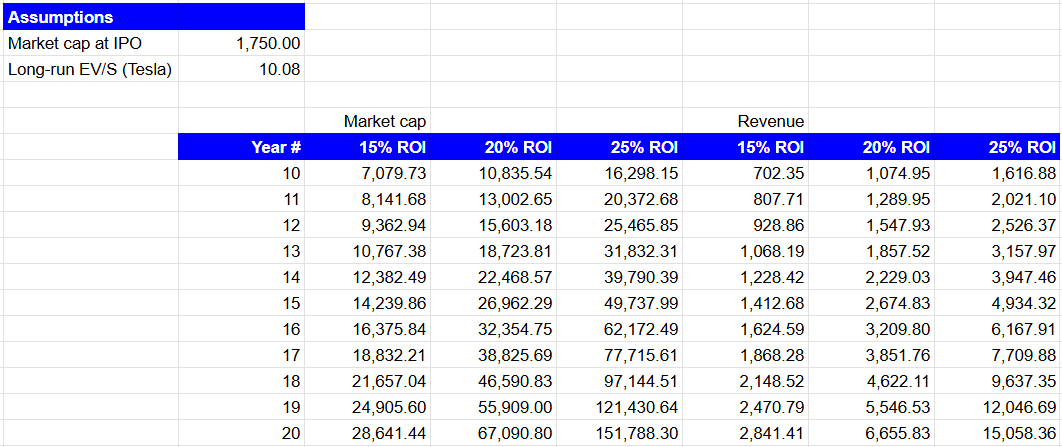

That won’t happen without revenue skyrocketing, with the exact number required depending on the long-run EV/S multiple. Using Tesla’s value of 10.08x (which conveniently factors in Musk’s insane productivity and the AI & hardware mix), required revenue falls between $702B and $1.6T:2

Only one company has ever reached that mark - Amazon, with its FY 2025 revenue of $717B, and whose founder is pouring resources into Blue Origin, the second launch operator in history to successfully reuse a rocket.

While this seems distant compared to SpaceX’s most recent $18.7B mark, it doesn’t completely defy statistics: 10 years ago, when Bezos was 52 (Elon’s 54 right now), and Amazon was 22, the company’s reported annual revenue was $136B, while Tesla’s most recent results were $95B in revenue (with $4B in net profit3).

The last piece of the valuation puzzle is the conditional probability that Musk can pull it off, expressed as P(Revenue > $702 billion | Multiple milestones jointly reached). If anything falls short and the revenue fails to reach the target, the model might crash back to Earth, together with realized returns for IPO investors.

What’s the single biggest thing that might go wrong? There are numerous stronger contenders for the largest segment of the TAM: the $22.7T enterprise AI market. Even if AI agents spread like wildfire, xAI has to win against Microsoft, OpenAI, Google, Anthropic, and Amazon, as well as vertical AI vendors like Salesforce, ServiceNow, Palantir, Oracle, and SAP.

While Musk can still out-innovate everyone over time, as he has already demonstrated with his multi-industry track record, relying on that assumption to achieve a bare 15% annual return makes little economic sense.

Our verdict

As Musk likes to say, the company’s mission is to make life multiplanetary and reach stars. Is making our civilization’s dream come true worth underwriting an obviously overpriced IPO? For non-financial reasons, many people would say “yes”, which guarantees oversubscription. For a rational investor, however, patience is a better strategy.

Given aggressive pricing, many factors need to align for this IPO to deliver good long-run performance, making the entire construction too shaky. Our verdict: if you want to ease the FOMO and support the mission, put a little, but if you want to make money, wait for a better entry price4.

The NASDAQ index averaged 15.65% over the period 1996 to 2026.

That means by Year 10, SpaceX’s revenue alone would need to surpass the current 2026 GDP of entire developed nations like Switzerland, the Netherlands, or Saudi Arabia.

Just for reference, NVIDIA sits at $216B in revenue and $130B in net profit.

A better entry price = a lower EV/S (closer to long-run AI comparables).