Innovative growth companies as the Holy Grail

Where to look for premier investment returns | Part 1

Summary

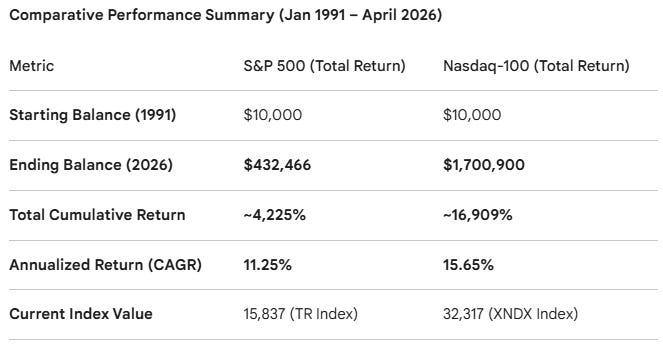

While there are myriad investment ideas and strategies, we focus on equity investments in innovative growth companies because this is where the best investment returns are found. For example, from 1991 to 2026 (which includes the Dotcom Bubble of 2000), the NASDAQ-100 produced an annualized total return of 15.65% vs. 11.25% for the S&P500. There are several fundamental economic reasons for such outperformance, which we explore below.

Equity outperforms all other asset classes

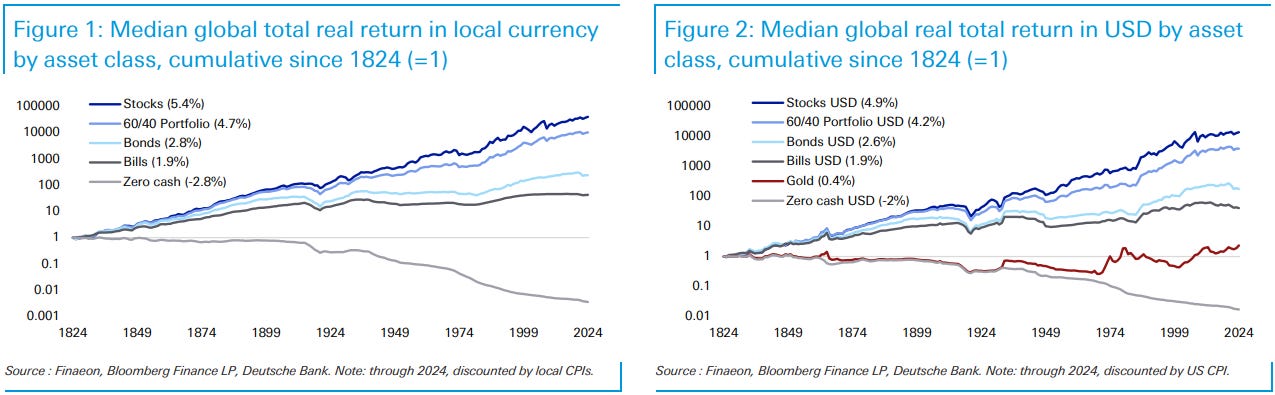

Have you ever wondered which is the highest-yielding asset class in the world? Equity, or ownership stakes in public and private companies, consistently outperforms everything else globally. This outperformance is well-documented by many research teams and papers: for example, the research report from Goldman Sachs or this 200-year data panel from Deutsche Bank:

Financial market economists call this statistical phenomenon an Equity premium puzzle and still debate why it exists. The reason is rooted in how the economics of returns work across all asset classes:

Cash simply doesn’t produce any yield.

Bills and bonds yield a risk-free rate + a risk premium (which is lower than an equity investor would demand since debt is inherently less risky).

Commodity prices tend to grow at the inflation rate (with occasional price spikes in some commodities that then revert to their average levels).

Real estate combines rental yields (roughly equal to fixed-income yields) and price gains (roughly equal to inflation). If we add them together, the resulting yield can be high, which may put pressure on the thesis, according to some data, but both those components are still bound to the aforementioned economic laws.

There are also cryptocurrencies, which have delivered unmatched performance since the creation of Bitcoin in 2009, but it might still be too early to say where they’re heading compared to traditional asset classes, which have been around for hundreds of years1.

At the same time, equity returns are linked to the profits of the underlying businesses, which tend to grow at the GDP growth rate but can often outpace it, as companies naturally fight for larger market shares and stock exchanges act as a selection mechanism to pick winners:

The global competition and the pursuit of greater profits both fuel capitalism to invest more and more resources in R&D, new technologies, means of production, the marketing of new goods and services, and distribution infrastructure. And equity is technically the only way to capture those ever-increasing profits and the primary source of first-generation wealth worldwide: 59% of millionaires made their first million through entrepreneurship (i.e., owning equity in a business). And almost all billionaires worldwide derive their wealth from ownership stakes in their own companies.

If we don’t want to start a (new) business yet want to have a tailwind for our returns, we should look at others’ businesses. We have to start looking inside the investable equity universe.

Revenue growth explains most of equity returns

Which direction do we go once we’re inside that universe? To answer that question, it’s worth understanding what the main driver of profit growth and hence equity returns is.

Shareholders want their companies to make money to survive and thrive. And making money requires selling products to customers. This brings revenue, which is the primary regular source of cash inflows. The cash is used to cover operating expenses and capital spending, which are the primary destinations of cash outflows. The difference between all outflows and all inflows available for distributions to shareholders through dividends and buybacks is called Free cash flow to equity (FCFE) and converges to accumulated net profits in the long run.2

If we divide net profits by revenue, we get what’s called the margin. Profits originate from revenue and flow to shareholders’ pockets through margin. Because margin can never exceed 100 percent of revenue and is typically lower in practice, the only way a company can accumulate large net profits is by substantially increasing its revenue. In 2014, researchers from BCG confirmed this intuition, and a team from Morgan Stanley arrived at similar results:

The result also extends into the future per J.P. Morgan’s Long-Term Capital Market Assumptions:

That doesn’t, of course, mean that profits are not important. At the end of the day, shareholders are expecting distributions, and without profits, there’s no free cash flow to pay those distributions from. We’re just saying that significant profits aren't possible without significant revenue.

On average, companies’ revenue grows at the same rate as GDP, which is 2-4% in most countries. If a company grows faster, that means it’s taking over some other player’s market share, represented by that player’s revenue divided by the total GDP. Because GDP is ultimately the sum of all spending in an economy, the company that wants to outgrow the market must fight to get a bigger share of that spending.

If we want higher returns, we should look more closely at growth companies that expand faster than GDP by taking over competitors’ market share.

Innovations are critical to outsized growth

If a company wants to win a larger share of customers’ budgets, it must introduce a superior new product at a better price, or it will struggle to lure customers away from their existing suppliers. Of course, unless it’s a monopoly, but today monopolies are battled and are considered rare.

To find a recipe for making superior products, we can look at entrepreneurs with consistent track records of creating them, of whom Elon Musk is the best example. In a video recorded at SpaceX HQ in 2017, Sam Altman, the then-CEO of Y Combinator, has the following dialogue with Musk:

Altman: How should someone figure out how they can be most useful?

Musk: Whatever the [product] is that you’re trying to create, what would be the utility delta compared to the current state of the art, times how many people it would affect? That’s why I think having something that makes a big difference but affects a small to moderate number of people is great, as is something that makes even a small difference but affects a vast number of people. Like the area under the curve of utility.

Not being useful is what kills most young companies (which die before growing into big companies, hence fewer big companies either), so this conversation directly relates to developing and launching new products. The marginal customer utility that such a product creates can be regarded as a formal definition of its superiority. How to achieve that superiority? By fostering innovations.

What is innovation? Basically, any practical implementation of a new idea that creates improvements in goods, services, and distribution. Rather than just occasionally innovating, companies should maintain a constant high pace of innovation:

Though Musk’s original commentary focused on technology companies, he later generalized it to apply to any company trying to stay ahead of the competition. Over time, the pace of innovations translates into a deep advantage of a company’s product over substitutes, enabling it to outsell and outgrow its peers.

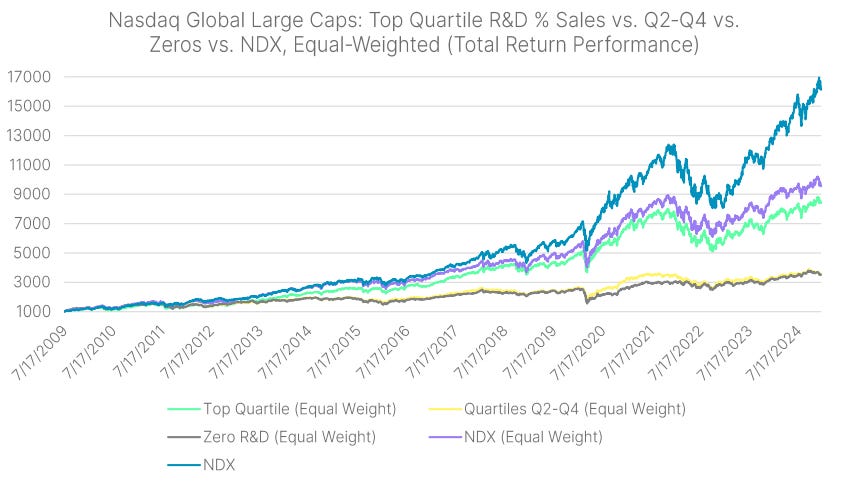

Indeed, the study by NASDAQ supports the hypothesis that companies that spend more on R&D (innovation) demonstrate higher shareholder returns:

The NASDAQ-100 index itself, widely known as a collection of innovative stocks, has significantly outperformed the S&P500 on a total return basis, even if we start to count before the Dotcom Bubble:

What’s the main driver behind innovations? We can learn the answer from an industry that made recognizing and supporting innovations its everyday business: venture capital investing. VCs argue that to produce more innovations, it’s critical to have outstanding people on a team, which they aim to capture by measuring the “talent density” of the startups they screen for investment. We’ll explore this idea in depth in our follow-up notes.

What’s next

The key takeaway for now is that to capture faster-than-average growth and premier investment opportunities, we need to identify companies with a high pace of innovation and a high density of talent. In our next article, we’ll explore where innovations and talent (and therefore growth) tend to concentrate, and how big the investment returns could potentially be3.

Also, the top 3 crypto billionaires are founders of Binance, Tether, and Coinbase, which are simply businesses in this new industry, and therefore belong to the equity asset class.

FCFE = Net income + D&A - Net CAPEX - dWC + Net borrowing

D&A eliminates Net CAPEX in the long run (since all equipment we buy depreciates). dWC converges to zero because, after the company's final production cycle, it no longer needs working capital. And the firm will aim to repay its debt (because debt has a fixed maturity). Hence, all terms converge to zero, except Net income.

One idea really worth covering is the variance of returns inside each asset class, how this feature is critical to achieving high absolute returns, and how equity beats other asset classes once again.

Tickers, I need tickers!